|

|

BVWire—UK is a free service from BVR focusing on the business valuation profession in the United Kingdom. We offer news and perspectives from valuation thought leaders, the High Courts, HMRC, the standard-setters, ICAEW, RICS, and more.

Please be in touch with your perspectives, news, and ideas—and pass this issue along to colleagues (complimentary sign-up instructions are here).

|

Global intangible asset value rebounds to hit

all-time high

Business valuers recognise that intangibles present individual ‘facts and circumstances’ challenges. And IFRS 3, even without the proposed amortisation changes, does not fully report the current value of acquired or created intangibles (increasing the operational value of intangibles is generally a strategic goal).

One place to look for benchmarks is the ‘2020 Global Intangible Finance Tracker’ (GIFT) study from Brand Finance. ‘GIFT 2020,’ released last week, takes issue with accounting standards (again) since they do not reflect fair value. David Haigh, CEO of Brand Finance, has been quite vocal on what he calls ‘the failure of IFRS 3 to adequately report the current real value’ of all intangibles. And, as Annie Brown, the author of the GIFT reports, writes:

Investors deserve better. They deserve better disclosure about internally generated intangibles, and they deserve a higher quality of the reporting of acquired intangibles. Reporting standards need to go further to guide boards to this greater transparency.

No wonder analysts struggle.

What can business valuers learn from ‘GIFT 2020’?

- Total intangible asset value has risen to an all-time high of $65.7 trillion, representing 54% of overall listed global value.

- Total intangible value is comprised of both disclosed intangibles and undisclosed intangibles. Within disclosed intangibles, the most valuable asset class continues to be goodwill, which represents approximately 8% of global value, at $8.8 trillion as of 1 September 2020.

- UK auditors are comparatively cautious about adding intangibles to listed company balance sheets. In fact, they’re not even in the top 10. The United States retains its crown as the most ‘intangible’ country based on listed entities, concludes the report.

- Despite the fact that many entities report goodwill that is higher than the total value of the company, only 10% took an impairment in the last 12 months.

- Intangibles are subject to market conditions and many other factors and don’t track well with any indicator of performance. Summarising this problem for financial analysts, GIFT 2020 quotes David Matthews, the president of ICAEW, who says, ‘I recognise the utopia where you could have the value of the balance sheet equate to the enterprise value, but I don’t think it is likely.’

- The biggest impairments this year? Schlumberger leads the list (at about $US9 billion), followed by HSBC, Procter & Gamble, and CenturyLink.

- Expect a big write-off in the first year when a new CEO and/or CFO takes over.

- Smaller enterprises are less likely to have major internally generated brand values, but the trend still follows that higher-valued companies tend to have higher undisclosed intangibles.

|

|

Concerned about a specific business valuation issue? The IVSC wants to know.

The International Valuation Standards Council’s (IVSC) Agenda Consultation to solicit input to help set the agenda for the future development of the International Valuation Standards (IVS) is open for another six weeks. ‘This edition provides an update on the previous Gap Analysis included in the IVS Agenda Consultation 2017 together with a summary of potential future topics in order to gain feedback on the valuation topics that stakeholders feel should be prioritised or added to the IVSC’s agenda,’ says the organisation.

Comments are due 15 January 2021. Feedback is wanted about valuation topics that the IVSC should address as part of its current agenda as well as additional valuation topics that should be prioritized or added to the agenda.

The IVSC plans to publish an Agenda Consultation on a triennial basis as part of their open consultative standard setting-process. |

|

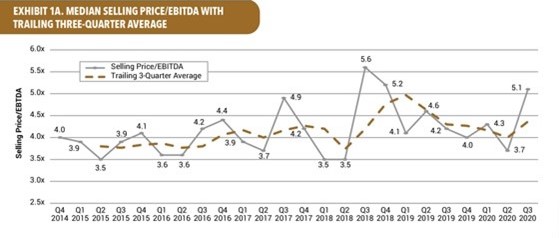

DealStats 3Q20 small private-company EBITDA multiples rise

After stalled M&A, lockdowns, and a pandemic, it’s easy to forget that small enterprise value was declining through most of 2019. EBITDA multiples (median selling price/EBITDA) were down already, as shown in the summary table, before hitting a low in the second quarter this year, at just 3.7x, according to BVR’s DealStats Value Index (DVI).

As we all know, deal volume for small companies dropped to ‘almost a standstill,’ says Adam Manson of BVR.

The third-quarter improvement was dramatic across all industries, rebounding to 5.1x—the highest level since 2018. ‘As the economy, and in particular, the M&A transaction portion, continues to recover, DealStats will continue to monitor the trends in the EBITDA multiple,’ says the report. |

|

Does COVID-19 alter the Companies Act, or the value of minority shares?

All business valuers accept the fact that minority shares hold discounted value. It’s understood that minority shares have reduced flexibility, fewer rights, and less access to cash-flow benefits.

BVWire—UK, therefore, noted a great COVID-19-era summary of the Companies Act from Slaughter and May lawyers Hayden Cooke and Murray Cox. Their summary reviews the rights and privileges accorded to different levels of ownership and can help financial analysts more clearly define why minority values should be decreased—often quite dramatically.

The Cooke and Cox analysis appeared earlier this year on lexology.com and is an extract from the upcoming Corporate Governance Review, 10th edition.

A selection of rights considered in their summary, all of which impact the relative discount appropriate to minority positions for UK enterprises, include such Companies Act rules as:

- Rights of shareholders holding as little as 5% of the voting rights to ‘requisition a meeting, and add any item to the agenda or add any item to the agenda for the company’s AGM’;

- Protections against secondary share offerings (by simple majority resolution) either via the Companies Act, or in practice guidelines observed by directors;

- Relative protections afforded shareholders regarding transactions such as incentive plans and major acquisitions;

- ‘Any proposal to acquire control (defined as 30 per cent or more of the voting rights) of a company subject to the Takeover Code requires an offer to be made to all shareholders on the same terms’; and

- Practical access to some listed company standards such as, in principle, the concept that information must be made available simultaneously to all shareholders.

Cooke and Cox also reference other UK rules that may indirectly influence the powers and discounts of shares held by minority owners, such as guidelines for institutional investors, the Listing Rules, and the Takeover Code. |

|

The goodwill comment period is extended for one last time, to 31 December

This discussion began in earnest in 2015 as part of the discussion paper ‘Business Combinations—Disclosures, Goodwill and Impairment,’ and the current question about the treatment of goodwill has been the subject of extensive discussion by ICAEW, IVSC, and international groups. Now, the International Accounting Standards Board (IASB) has extended the comment period to 31 December.

The IASB started with the assumption that goodwill is not always recognised in a timely fashion and that disclosures required by the IFRS standards are insufficient or potentially confusing. Concern has also been expressed about the cost and risk of the current impairment testing model. Leaders of the business valuation and auditing professions have had a wide range of responses already, but most seem to argue that the current impairment model offers more benefits than a ‘wasting asset’ amortisation alternative.

However, most of the feedback IASB received so far has raised concerns with alternative models. Perhaps the most forceful response came from a very long comment letter the CFA Institute prepared and sent to the US FASB. Among other things, the comment letter suggests that amortising the trillions of pounds of goodwill on global balance sheets would dwarf the total value of corporate profits for several years. |

|

Dates for your diary

1 December (today): The Absence of a Size Effect: Letting Go of the Size Premium Featuring: Clifford Ang (Compass Lexecon) 18:00 BT

1 December (today): ICAEW Practical Business Valuation, virtual, four-day course

17 December: Transfer Pricing: 2020 Year-End Considerations, a Lexology webinar with Mark Alms, Alvarez & Marsal, 14:00 BT

21-22 December: Excel Modelling—Investment Appraisal, Valuation, and Business Cases, virtual |

Want to share a news item? Have feedback or comments? Please contact

David Foster at ukeditor@bvresources.com. |

|

|

|

Business Valuation Resources, LLC

111 SW Columbia Street, Suite 750, Portland, OR 97201 U.S.A.

+011-503-479-8200 | info@bvresources.com

© 2020. All rights reserved.

|

|