|

|

BVWire—UK is a free service from BVR focusing on the business valuation profession in the United Kingdom. We offer news and perspectives from valuation thought leaders, the High Courts, HMRC, the standard-setters, ICAEW, RICS, IVSC, and more.

Please be in touch with your perspectives, news, and ideas—and pass this issue along to colleagues (complimentary sign-up instructions are here).

|

Long-term growth rate assumptions for terminal values can cause exit multiple mistakes

DCF models are becoming more accepted in UK business valuations, and several experts note that mistakes happen when analysts don’t consider the reasonableness of the implied long-term growth rate embedded in the selected exit multiple. For most businesses, it’s unlikely that the growth rate during the next few years will be sustained at exit or in a terminal value calculation—though owners and investors often wish it was. In fact, both the growth rate and the valuation date multiples calculated at the valuation date nearly always need to be reduced because of the increased risk and uncertainty of cash flows in the future (typically, three to five years in many DCF analyses).

Jim Hitchner, the US-based valuation expert, prepared the following table of the long-term growth rates to support exit multiples of 3 to 8 in the current edition of his Hardball With Hitchner newsletter. It’s extremely rare that any company exceeds the economic growth rate in perpetuity after five years, so, referring to Hitchner’s analysis, a growth rate assumption implied by an exit multiple higher than 3 would seem optimistic. Still, the M&A market would balk at such a low exit value in any projection, where often 8 times EBITDA seems to be the floor, and higher multiples are frequently assumed.

Exit multiple derived from listed comparables |

Implied long-term growth rate |

3 |

2.9% |

4 |

6.7% |

5 |

9.1% |

6 |

10.8% |

7 |

12.0% |

8 |

12.9% |

Hitchner points out that higher assumed exit multiples create the situation where “the terminal value is higher than the present value of the interim cash flows.”In these valuations, it could be argued that the single biggest determiner of value in a DCF analysis is the financial expert’s terminal growth rate assumption.

The Footnotes Analyst also examined the exit multiple problem in a series of articles last month. “If a valuation multiple, such as EV/EBITDA, is used to calculate a DCF terminal value, the multiple should reflect expected business dynamics at the end of the explicit forecast period and not at the valuation date,” the authors say. “This is best achieved by basing the exit multiple on forward-priced multiples for the selected group of comparable companies,” which they demonstrate with a series of examples. They also include an interactive model that business valuers can employ to calculate their own DCF terminal values using forward-priced multiples. |

|

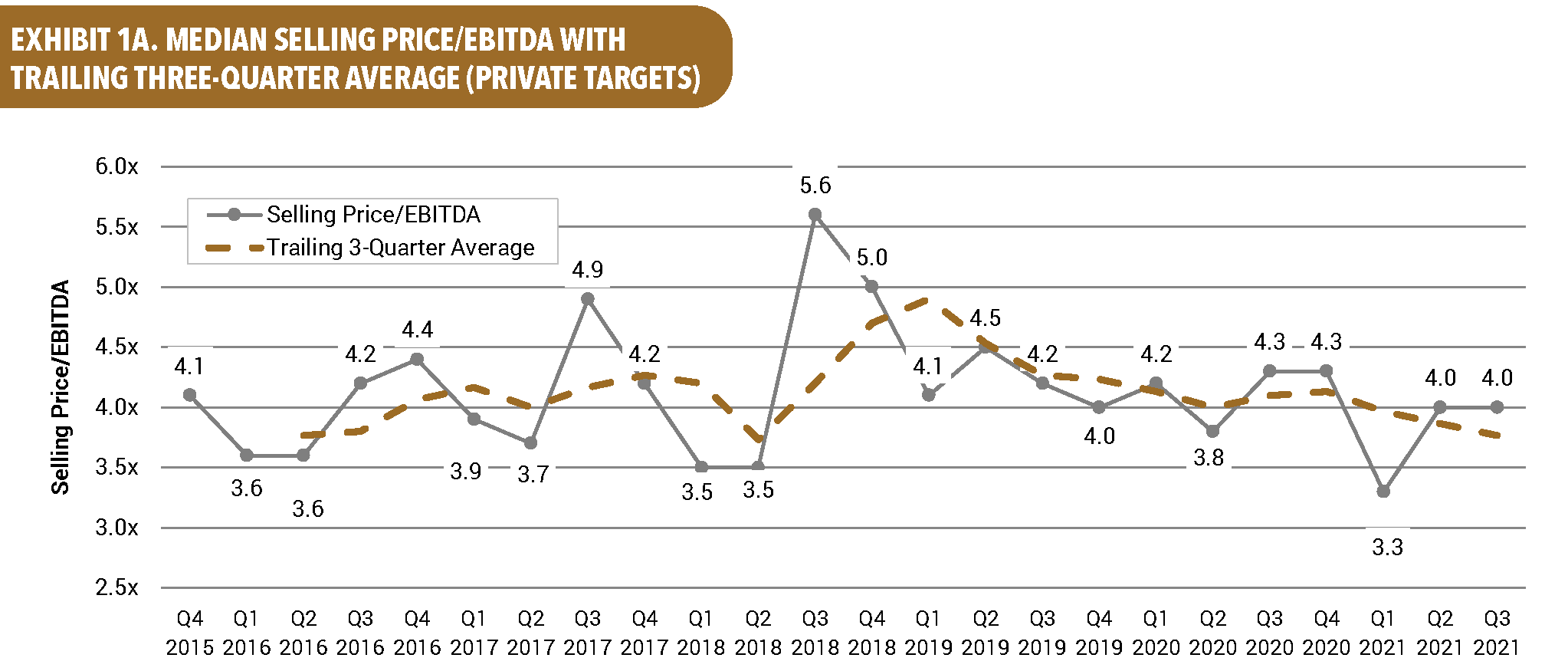

SME transaction values stay steady at 4.0x for 3Q2021

According to the latest issue of the DealStats Value Index (DVI), which calculates valuation multiples and profit margins from closely held companies each quarter, as shown in the table, EBITDA multiples are at 4.0x for the third quarter of 2021, which is unchanged from the rate in the second quarter of 2021.

The 4Q 2021 DVI highlights the trend in the EBITDA multiple since 2015 and reports lower multiples than those available from private equity or investment banking sources, so they’re far more reflective of fair market value calculations than synergistic or financial sector pricing.

The chart also highlights the median selling price/EBITDA with the trailing three-quarter average over a five-year period. Download the current issue of DVI to see all of the new trends in private-company transactions.

|

|

UK job listings for contentious disputes managers and associates increase

BVWire—UK notes an increase in job postings for business valuation managers. The leading job boards are showing more postings for contentious valuations managers or associate directors this month, indicating increased demand from some of the high-profile disputes. The increased postings all require candidates with valuation dispute experience and typically prefer ACA or ACCA qualifications. Specialisms, mentorship with experienced partners, and international career advancement are typically included in these listings as benefits, as is a diverse set of complex project work including damages valuation, mediation, competition disputes, intellectual property/intangibles analyses, purchase agreements, and family or tax engagements.

There may be more demand for client-facing managers who can lead junior analysts than supply for these opportunities, so promises of working on high-profile cases, directly with partners and clients, are common in the current listings. |

|

UK require more complete disclosures of beneficial ownership interests beginning in January

Global standards are hoping to create further disclosures of beneficial ownership of trusts and other entities to reduce cross-border fraud and tax avoidance. The UK’s response to these reforms mostly becomes effective in January, which should make it easier for forensic and business valuation experts to track hidden assets.

To do this, the UK has enhanced the process of collecting and disclosing information on people with significant control (PSCs) via the Small Business, Enterprise and Employment Act in 2016. Initially, reformers wanted the corporate register to show the name of the trust, the trustees, and the beneficial owners of the trust. While only true in a small minority of schemes, an argument was successfully made that the publication of such names might expose vulnerable beneficiaries.

The reformed rules, therefore, call for the corporate register, where the beneficial owner is a trust, to provide public access (not only access by the competent authorities at HMRC and elsewhere) to:

- The names of the trustees; and

- Only anyone who has the “right to exercise, or actually exercises, significant influence or control over the activities” of the trust or company.

The regulations require UK LLCs, LLPs, and overseas holding companies to hold information on their own beneficial ownership and to respond to any reasonable public request for information from the register as well as file beneficial ownership information with the national registrar of companies.

Perhaps as importantly, Jersey, Guernsey, and the Isle of Man have confirmed that they will voluntarily adopt public registers of beneficial owners by 2023, providing a further source for financial experts who need to identify the ownership of hard-to-track business assets. |

|

iiBV update on-demand global BV core courses

BVR and the International Institute of Business Valuers (iiBV) have completed the current updates of their core Advanced Business Valuation course. The five e-learning modules qualify for iiBV 210, 211, 212, 213, and 214 credits, which align with the current International Valuation Standards from IVSC. The five modules are: Valuing Intangible Assets, Valuing Early-Stage Companies, Valuing Minority Interests, International Cost of Capital, and Black-Scholes Option Modelling. |

|

CFA Institute repeats support for continued goodwill impairment models

“Amortisation over a straight-line period tells you nothing. Impairment … says that something you acquired didn’t turn out, and users of financial statements should ask more questions,” Sandra Peters, head of financial reporting at the CFA Institute, said at last month’s Calcbench webinar.

The webinar, What’s New in Goodwill, is available free on YouTube and featured Peters along with VRC co-CEO PJ Patel and Calcbench CEO Pranav Ghai. Peters was previewing CFAI’s current survey of members, which finds broad support for the traditional testing of goodwill for impairment—and skepticism about U.S. FASB efforts to change to straight-line amortisation (other international regulators appear to be moving away from the amortisation idea, so both preparers and users of financial statements could end up with separate versions).

The CFAI and Peters, of course, are concerned about the investment professionals and the information they derive (or fail to derive) from listed company financial statements. She says that, in practice, many CFAs perform their own impairment analysis with much less information than the companies have, suggesting it is valuable to them and may not be as onerous and costly as proponents of amortisation suggest.

Business valuers at the big firms who conduct impairment tests know how difficult they are, but it is the one part of the audit process that requires pushback on optimistic forecasts for acquisitions that may be underperforming. |

|

Dates for your diary

8-11 November: IMAA’s Damodaran on Valuation, live—online

1-9 December: Practical Business Valuation, ICAEW live—online (four sessions) 09:30-12:30 BT

13-17 December: US AICPA Virtual Business Valuation School, live—online

3-5 October 2022: 12th Annual International Valuation Conference, Riyadh, Saudi Arabia

Want to share a news item? Have feedback or comments? Please contact David Foster at ukeditor@bvresources.com. |

Want to share a news item? Have feedback or comments? Please contact

David Foster at ukeditor@bvresources.com. |

|

|

|

Business Valuation Resources, LLC

111 SW Columbia Street, Suite 750, Portland, OR 97201 U.S.A.

+011-503-479-8200 | info@bvresources.com

© 2021. All rights reserved.

|

|