|

|

BVWire—UK is a free service from BVR focusing on the business valuation profession in the United Kingdom. We offer news and perspectives from valuation thought leaders, the High Courts, HMRC, SSBV, ICAEW, IVSC, and more.

Please be in touch with your perspectives, news, and ideas—and pass this issue along to colleagues (complimentary sign-up instructions are here).

|

IVSC offers further perspective on brand valuation standards

The International Valuation Standards Council (IVSC) has released “Rethinking Brand Value,” the third in a series of perspective papers on intangible assets. Part 3 takes a deeper dive into brands and reputation value creation by:

- Examining how brands generate value for organisations and the attributes of such value creation;

- Analysing how investors assess the enterprise value creation attributable to brands; and

- Discussing the value measurement techniques and assumptions used to estimate the value of brands.

Parts 1 and 2 of the series examine the “Case for Realigning Reporting Standards With Modern Value Creation” and took a deep dive into human capital value creation and measurement. |

|

Transcript of ‘financial experts in the UK courts’ presentation available

Andrew Strickland has provided the speakers’ outline for his recent presentation on decisions that address the role of financial experts in the UK courts. This new presentation addresses two significant cases that have arisen since his last summary in 2020.

Strickland notes the theme running through his entire update is the special power that is vested in an expert. He first refers to the recent FTAI AirOpCo UK and Olympus Airways [2022] EWHC 1362 decision. Olympus attempted to use their own employees rather than independent experts—and “the judge profoundly disagreed.”

He also warns all business valuers in the UK of the risks of careless work, referring to Liverpool Victoria and Dr Zahar [2020] EWHC 846 and a number of other new cases. Strickland says, “[T]he expert witness who falls a long way short of the standards expected can expect direct, bone-crunching, career-disrupting criticism.”

Further cases examine excess coaching of expert testimony, the value of trademark infringement, and further business valuation topics.

The outline can be downloaded from BVR here. |

|

New family court decision limits reporting restriction orders

Should financial remedy analyses be routinely anonymised when business assets are valued? A new family court judgement, Gallagher v. Gallagher (No.2) (Financial Remedies) [2022] EWFC 53, says no.

In this matter, the husband applied for a reporting restriction order (RRO) on five grounds, including the fact that a significant proportion of the final hearing focused on the valuation of a construction business in which he was a joint and equal shareholder. It was argued that dissemination of this information would also harm third parties including his business partner, could expose him to HMRC actions, and would unfairly prejudice the court.

The family court concluded these proceedings did not fall within s.12 of the Administration of Justice Act 1960, which are heard in private under FPR 27.10, saying that the intent was to provide partial privacy at the hearing only—which does not necessarily offer confidentiality for financial remedies. “In my judgement the mantra ‘we have always done it this way’ cannot act to create a mantle of inviolable secrecy over financial remedy proceedings which the law, as properly understood, does not otherwise recognise,” the family court ruled. |

|

Investors are returning to free cash-flow analyses. Do they agree on what that is?

Market corrections in London and across the globe have changed the dialog for equity analysts, argues Aswath Damodaran in his most recent blog post. “There has been more talk of earnings than of revenue or user growth this year, and the notion of cashflows driving value seems to be back in vogue.”

Unfortunately, he continues, “Free cash flow is one of the most dangerous terms in finance, and I am astonished by how it can be bent to mean whatever investors or managers want it to, and used to advance their sales pitches.”

Damodaran suggests that the investor community should return to the basics as defined by business valuation standards and practices.

I believe that any measurement of free cash flow has to begin with a definition of to whom those cash flows accrue. Since a business can raise capital from owners (equity) and lenders (debt), the free cash flows that you compute can be to just the equity investors in the business, in which case it is free cash flow to equity, or to all capital providers in the business, as free cash flow to the firm.

|

|

OECD releases final fiscal valuation guidance for crypto-assets

The Organization for Economic Cooperation and Development (OECD) published the final Crypto-Asset Reporting Framework (CARF) on 10 October 2022. This provides for the automatic exchange of information between countries on crypto-assets. These are intended as global standards, though the U.S. likely will not adopt them, and it’s left to individual countries to apply them within their own jurisdictions.

The final CARF provides some guidance on hard-to-value assets. They allow analysts to rely on the second value of new resulting property if the hard-to-value asset is exchanged. In addition, if the relevant crypto-asset service provider does not maintain an applicable reference value, it may rely on:

- First, the internal accounting book values with respect to the relevant crypto-asset should be used;

- If a book value is not available, a value provided by third-party companies or websites that aggregate current prices of relevant crypto-assets must be used if the valuation method used by that third party is reasonably expected to provide a reliable indicator of value;

- If neither of the above is available, the most recent valuation of the relevant crypto-asset must be used; and

- If a value can still not be attributed, a reasonable estimate may be applied as a measure of last resort.

Prior to the release of the final rules, based on responses to the initial March 2022 draft, the OECD revised many provisions including the definition of covered assets, the treatment of decentralised finance (DeFi) platforms, and who would be required to report. The final rules include a new threshold of $US50,000 for retail transaction reporting. |

|

RICS BV working group release restricted stock valuation guidance

It’s been a good autumn for draft guidance from the valuation professional organisations. Following up on the draft guidance from the US AICPA on business combinations last month, the RICS Worked Example Group (WEG) released its new exposure draft on the valuation of growth shares in the UK. Comments are now welcome. Details of the exposure draft and how to submit responses are available at the WEG website at sharevaluationweg.org. |

|

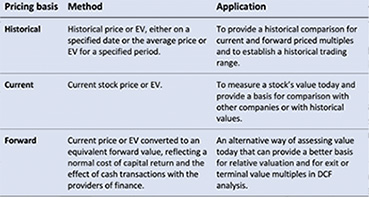

New study recommends a combination of historical, current, and forecasted results to improve valuations

Will forward-looking estimates provide financial experts with the best valuation multiples? Most business valuation leaders make that assumption, since the estimated future benefits of ownership ultimately determine value. The authors of The Footnotes Analyst offer a new perspective in their recent post. In “Equity Analysis Using Price-Multiple Charts,” they suggest that historical, current, or forward prices “individually provide valuable insights but combining them provides a bigger picture and facilitates further analysis.”

Their summary of pricing bases appears in the chart below.

The authors have studied valuation calculations extensively, most recently in two other posts:

Summary of Alternative Pricing Bases for Valuation Multiples

|

|

Sign up now to subscribe to the new European Business Valuation Magazine

In September, the European Association of Certified Valuators and Analysts (EACVA) and IVSC launched the new European Business Valuation Magazine (EVBM) for valuation practitioners. You may download the first issue and subscribe to future quarterly editions for free.

The EBVM aims to increase the transparency of valuation practice in European countries and to enable professional exchange on an international level.

Issue one includes articles on: “Valuation Ambiguities Under the European Directive on Preventive Restructuring Frameworks,” business models, “Use Cases and Analytical Approaches for Valuation of the Asset ‘Data,’” and “Unlocking the Value of ESG.”

If you would like to submit an article for the magazine, then you can email the editors. |

|

Dates for your diary

8 November: Wilberforce Fraud, Trusts & Asset Recovery Conference, London and virtual

10 November: Prevailing in an Unpredictable Market: The 15th Annual Houlihan Lokey Alternative Asset Valuation Symposium, New York City

14-16 November: CIMA & AICPA Forensic & Valuation Services Conference, Las Vegas

15 November: ICAEW Forensic & Expert Witness Conference 2022, virtual

1 December: ICAEW Practical Business Valuation, four days, virtual classroom

7 December: Society of Shares & Business Valuers’ Causation and Financial Losses: Factors to Consider With Prem Lobo, London and virtual, 17:30-19:00 BST |

Want to share a news item? Have feedback or comments? Please contact

David Foster at ukeditor@bvresources.com. |

|

|

|

Business Valuation Resources, LLC

111 SW Columbia Street, Suite 750, Portland, OR 97201 U.S.A.

+011-503-479-8200 | info@bvresources.com

© 2021. All rights reserved.

|

|