|

|

BVWire—UK is a free service from BVR focusing on the business valuation profession in the United Kingdom. We offer news and perspectives from valuation thought leaders, the High Courts, HMRC, the standard-setters, ICAEW, RICS, and more.

Please be in touch with your perspectives, news, and ideas—and pass this issue along to colleagues (complimentary sign-up instructions are here).

|

New BVU article notes increased use of discounted cash flow in UK business valuations

‘There had been a consistent thread running through UK Court decisions of a preference for broad professional judgement over mathematical precision,’ says Andrew Strickland (FCA) in his new analysis, which appears in the July issue of Business Valuation Update. ‘The Judiciary appeared to recoil from any evidence which resulted in too many figures on the page. The greatest Jurists were known for their incisive legal wisdom rather than for their numeracy.’

In ‘A Quiet Revolution Is Going On in DCF Techniques in UK Cases,’ Strickland comments on the ‘long shadow into the future’ created by Practical Share Valuation by Eastaway and others. The book was updated in 2014 and again last year, but it’s particularly the 2009 original edition that stated ‘subjectivities within both the projections and also the discount rates’ caused the courts to reject the method.

‘As recently as the 2015 Tax Tribunal case of N Green and HMRC, Eastaway was used to ‘try and bludgeon a valuer who had the temerity to apply DCF within his valuation conclusions,’ Strickland recalls.

In the last 10 years, an initial cautious trickle of valuers using DCF in litigation work has broadened—in tax decisions, in shareholder disputes, and in contractual litigation.

Strickland credits this quiet revolution to ‘two forces:

- ‘Firstly, the desire of valuers to use various methods, including DCF, in their contentious valuations in the same way as they apply it in non-contentious work;

- ‘Secondly the inescapable realities of the valuation models used by private equity houses and others when valuing target companies.’

The BVU article reviews the successful use of the DCF in litigation, beginning with Saltri III and MD Mezzanine—the Stabilus Case in 2011. Strickland also considers several post-acquisition dispute cases such as Ageas v Kwik-Fit (GB), Hut Group v Cookson, Sycamore Bidco v Dunedin, and Triumph Controls v Primus International. DCF also appears in an increasing number of shareholder disputes, such as Arbuthnott v Bonnyman in 2015, VB Football Assets v Oyston, and others.

Strickland says that DCF is just the start. ‘The use of the capital asset pricing model is now featured in written decisions’ including a lengthy discussion of beta in Saltri III v MD Mezzanine and further analysis in the 2019 case of Burnden Holdings v Fielding. |

|

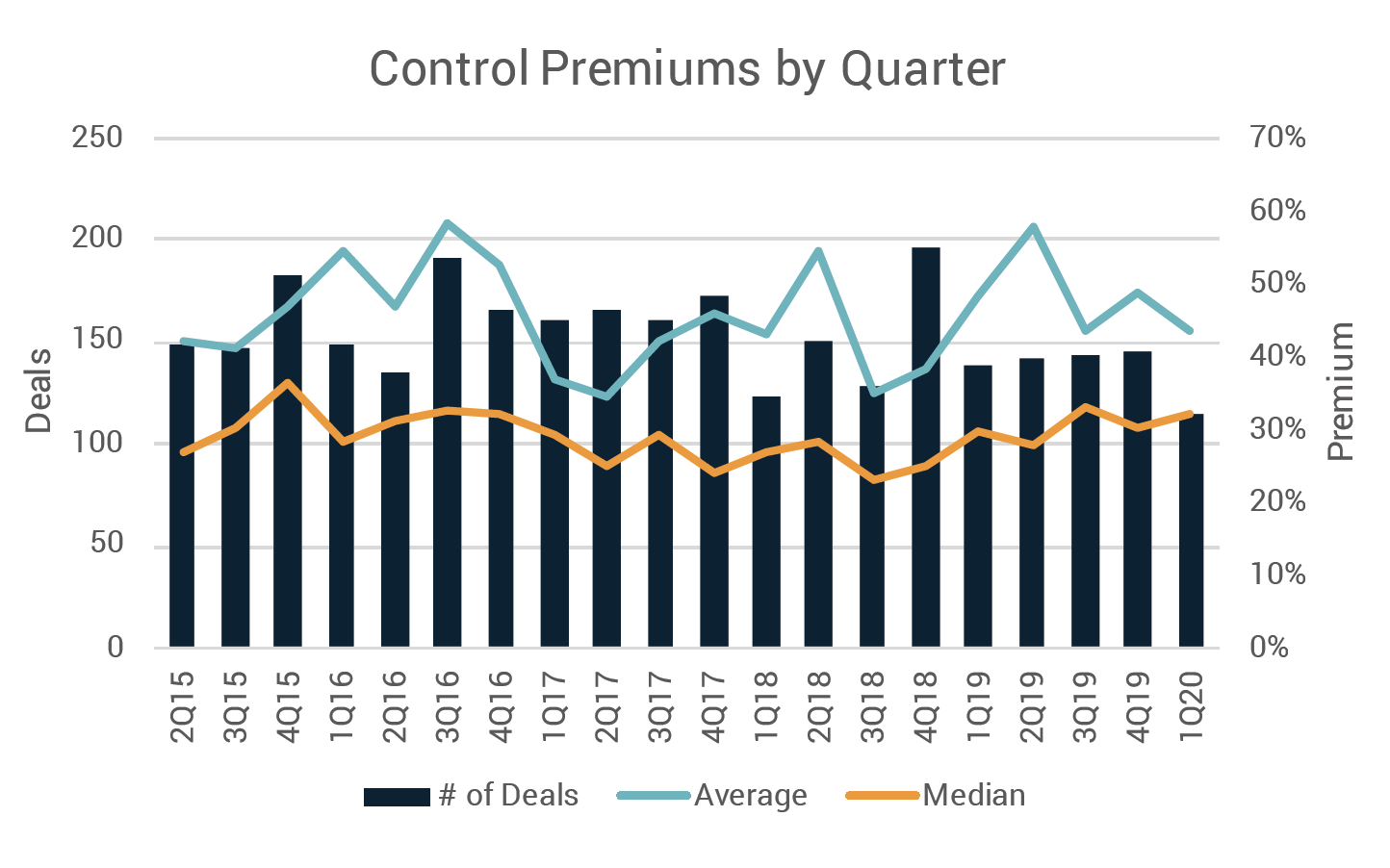

BVR/FactSet Control Premium Study updated for first quarter

The 1Q 2020 Control Premium Study report is now available, and we have updated the online FactSet Mergerstat/BVR Control Premium Study platform to include the latest analyses. Beginning with the first-quarter issue for 2020, the Control Premium Study has added several new charts and graphs that provide analysis on control premiums and minority discounts by industry sector, percentage acquired, deal size, strategic and financial buyer breakouts, method of payment, transaction multiples, and many more.

For non-US transactions, the average control premia was 26.8% during the quarter prior to the material outbreak of COVID-19, with a median of 20.0%. These premia were significantly lower than the rolling 12-month historical average, at 35.9% and 23.5%, respectively, for all transactions. The chart below shows the average and median control premia from 2Q 2015 through 1Q 2020.

The report also notes that, despite COVID-19, deal volume held steady in May.

|

|

More concern about the validity of the size premium factor

Most business valuers consider a size premium when calculating cost of capital for financial reporting purposes. It’s a key element of buildup method analyses in the Duff & Phelps Navigator and in other sources. Since the ‘famous’ Rolf Banz article in 1981, however, the idea that smaller firms demand higher returns has been questioned.

A new publication in the US legal website Law360 summarises the finance research since Banz’s article and argues that this practice should end. In ‘It’s Time for Valuation Experts to Let Go of the Size Premium,’ Clifford Ang (a senior vice president at Compass Lexecon) reconfirms the fact that, from 1982, immediately after Banz’s article, until the end of 2019, small stocks did not outperform larger stocks (that fact has accelerated during the rush to big stocks driving the FTSE now). Ang uses the value-weighted portfolio returns data from Dr. French’s decile size portfolio.

Ang is not the first analyst to make this point (he quotes Damodaran, speaking at the most recent CFA Institute annual conference, to the same effect). The changing returns profile of the major markets since the 1980s is one of the key reasons analysts can choose custom start years when doing cost of capital analyses in BVR’s Cost of Capital Pro. Ang argues that, lacking theory and statistical support, size premia should only be applied in a ‘facts and circumstances’ manner. |

|

How would a wealth tax impact business valuation?

The FT ran a long interview with Gus O’Donnell last week, saying that ‘a UK wealth tax is more likely than ever because of the reordering of politics caused by the coronavirus pandemic.’ Several other public figures have also discussed the impact on inequality from COVID-19, accelerating an existing problem.

O’Donnell, the former cabinet secretary under David Cameron, Gordon Brown, and Tony Blair, is quoted in the FT as saying:

You’ve got a Conservative party and prime minister talking about the red/blue wall. How to get to the forgotten man. We’re talking about FDR [Franklin D Roosevelt]. One nation conservatism. Lots of different things suggest to me that there might be more of an appetite for [a wealth tax] than you might have thought.’

Labour would follow, of course, freed of the label of being socialist, O’Donnell opined.

Calculating the impact on business value caused by a recurrent net wealth tax raises some interesting theoretical challenges, and the decrease would be less than upward adjustments in taxes from private investment. Suffice to say, during these current debates, a wealth tax would influence returns expectations.

Private UK wealth, in absolute money terms and relative to income, has risen sharply, and the current ‘levelling up’ spending program demands new ways to raise revenue. Time will tell. |

|

What do auditors expect from business valuation forecasts during COVID-19?

Auditors around the globe will be expecting multiple forecast scenarios in reports from their valuation experts. So agrees the panel on the newest iiBV June 2020 Update—COVID-19 Webinar. It’s a great discussion, well worth the time of any business valuer who does work for the Big Four in the UK. Led by Michael Badham, executive director of the International Institute of Business Valuers (iiBV), the panel (which is free), consists of: Yann Magnan, IVSC European Board chair (UK); Andrew Ooi, partner at Deloitte (Southeast Asia); Carla Nunes, Duff & Phelps (USA); and David Pearson, Leadenhall (Australia).

A practical approach to managing the market and income approaches during this period is also available from Dan Van Vleet’s programme for BVR in late June. Van Vleet and his colleagues offer multiple examples so that business valuers can continue to use these core BV methods without fear of ‘double counting or ignoring the current market impairment.’ If the comparables or benefit stream you’re measuring against are not impaired, then valuers must use pre-COVID-19 metrics for their target company to maintain an ‘apples to apples’ comparison, the programme demonstrates.

The iiBV panel discusses a number of current valuation topics, including asset impairments, projections, cost of capital, and more. This panel discussion follows up on its first webinar, iiBV’s Impact of COVID-19—Global Perspectives, which was released in April. |

|

Dates for your diary

10-13 July: ICVS-A Advanced Studies in Financial Instruments, virtual training

22 July: IVSC Standards Boards Update on Future Programmes, 14:00-15:00 BST, virtual conference call

9-11 September: BVR/AAML Virtual Divorce Conference, virtual event

11-13 October: American Society of Appraisers International Conference, virtual event

14-16 October: IVSC AGM 2020, virtual event with further information to follow

29-30 October: EACVA 14th Annual Business Valuation Conference, Munich |

Want to share a news item? Have feedback or comments? Please contact

David Foster at ukeditor@bvresources.com. |

|

|

|

Business Valuation Resources, LLC

111 SW Columbia Street, Suite 750, Portland, OR 97201 U.S.A.

+011-503-479-8200 | info@bvresources.com

© 2020. All rights reserved.

|

|