|

|

BVWire—UK is a free service from BVR focusing on the business valuation profession in the United Kingdom. We offer news and perspectives from valuation thought leaders, the High Courts, HMRC, the standard-setters, ICAEW, RICS, IVSC, and more.

Please be in touch with your perspectives, news, and ideas—and pass this issue along to colleagues (complimentary sign-up instructions are here).

|

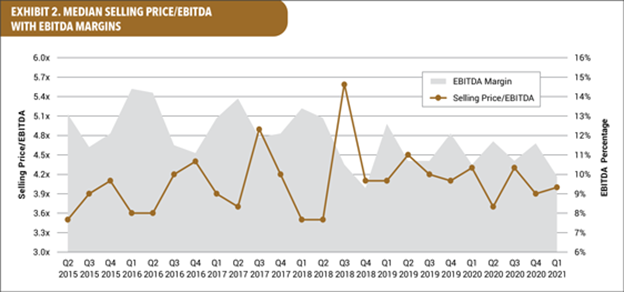

Deal prices for private equity transactions stay high—but are the underlying assets

less profitable?

The new DealStats Value Index Digest notes a worrisome trend: The average EBITDA margin of deals completed last quarter dropped. With a lower pretax profit number, deal values also fell.

From the second quarter of 2019 through the fourth quarter of 2020, EBITDA margins had seen very little change, coming in at 11% or 12% in each quarter. The move downward to the current 10% (see the table below) in 1Q2021 indicates that the duration of COVID-19 and the economic lockdowns have had a negative impact on small businesses despite the availability of continued government stimulus schemes and cost-control measures. Though DealStats data are primarily sourced from North American transactions, these conclusions can still support UK valuers as they prepare income forecasts that may be more conservative.

BVWire—UK subscribers may download the entire DealStats Value Index Digest for free.

|

|

MarktoMarket finds 82% minority discount for beer enterprise

Timothy Taylor & Co, the traditional British brewer and pub owner, recently transferred a 10% share of the business. MarktoMarket compared the pricing of this deal to the two large brewer-only deals: Camden Town and Meantime. The three companies had different capital structures, growth rates, and other business characteristics. Camden Town and Meantime were acquisitions of 100% of the share capital. Compared to these transactions, the new analysis found an 82% minority position discount for the 10% purchase.

As MarktoMarket co-founder Doug Lawson explains:

Conventional wisdom dictates that a minority stake should be discounted relative to a controlling stake to reflect the lack of control. This discount should be inversely proportionate to the size of the stake being transferred to reflect the fact that the rights of the shareholder become more limited as the position size reduces. This approach is generally accepted, however, the quantum of the discount is the subject of much conjecture.

MarktoMarket’s estimated enterprise value/EBITDA multiple for Meantime was 32x; our estimate for Timothy Taylor was 5.7x, a discount of 82%.

MarktoMarket collects data on both M&A and minority deals in the UK. Most of these minority transactions go unannounced.

For more details on these deals and MarktoMarket’s broader datasets, please contact Doug Lawson. |

|

‘Wells sharing’ may still be the least painful resolution in family law disputes with

shared ownership

UK family law courts are generally loathe to force the sale of a business to satisfy the debts of a shareholder resulting from a divorce settlement. Most couples who share interests in a company aren’t aware of this preference, and, even with the UK’s new no-fault standards, it’s common to find divorcing clients that are anxious about whether they’ll lose the source of the cash flow that’s supported them for years.

As Melissa Deutrom and Aaron O’Malley of Herrington Carmichael LLP write in an article last week:

A company is what is known as a “separate legal entity” … and there is said to be a “corporate veil” or barrier between the company itself and the company’s owners (its shareholders). Generally speaking, this means that the court would be unlikely to order a company to transfer or sell assets as part of financial proceedings stemming from divorce. This is because such assets are owned by the company and not by the spouse, and the company is not usually a party to such divorce proceedings.

As business valuers know, courts are less reserved about ordering the transfer of assets owned by one of the parties to the other party in a divorce, including the transfer or sale of the shares of a private company. Duetrom and O’Malley stress that the valuation issues become even more complex if an uninvolved spouse is a shareholder already or has other roles within the enterprise.

The new article offers a clearheaded examination of the common solution the UK courts use called “Wells sharing” (after the case Wells v Wells [2002] EWCA Civ 476). The courts order transfer of shares from one partner to the other without liquidating them.

In the original Wells case, the judge was unable to value a shared-interest firm that had declined into operating losses after the couple separated. The appeals court found that the income from the business was uncertain. The solution was to leave both parties with retained shares. “Retaining an interest in a company alongside your former spouse may be far from desirable for some parties—however, this would mean at least, that both parties would be subject to either increase or loss as a result of economic downturn,” the authors say.

Other valuation options: This new analysis describes some of the variables available to family law courts in such situations, including:

- Fixing a value for the shares in a company as an offset against other assets. Of course, valuing shares in a company is not always as simple as we would hope, particularly during times of economic uncertainty.

- With the support of business valuation experts, reducing the value attributed to the company and awarding more shares when the risk or uncertainty is high.

- Considering minority discounts when the spouse does not have control of the company.

- Considering whether the assets are truly “operating” or just held in trust by the company. The authors cite Akhmedova v Akhmedov [2018] EWFC 23.

- Including provisions within the company’s constitutional documents (i.e., the Articles of Association), or within a shareholders agreement, which provide for what is to happen to the shares in a divorce situation.

|

|

Gallagher survey anticipates higher contingent liabilities from litigation

Two-thirds of UK businesses expect litigation claims to remain at a high level or to increase this year, with 56% having faced accusations of unlawful behaviour in the last five years. Gary Fletcher, south managing director at Gallagher, says: “Litigation is being fuelled, in part, by supply chains, COVID-19 and Brexit but in addition to this, economic downturns also usually produce a boom in disputes.”

The survey suggest that the largest proportion of risks will come from employment-related claims as the Coronavirus Job Retention Scheme ends in two months.

Other prime sources of contingent liabilities come from outstanding debts, alleged contractual breaches, claims against insurers for failing to honour business interruption claims, or alleged infringement of intellectual property rights.

The survey results were reported at longdonlovesbusiness.com. |

|

What market risk and risk-free rates are your UK peers using now?

The average market risk premium UK analysts use was 5.6% in May, according to “Market Risk Premium and Risk-Free Rate Used for 88 Countries in 2021,” the latest research from Pablo Fernandez, Sofia Bañuls, and Pablo Fernandez Acin. The median was 5.7%, and this compares to a 5.5% average rate reported by valuation professionals in the U.S.

This paper contains the statistics of a May 2021 survey about the risk-free rate (RFR) and the market risk premium (MRP). By June 3, 2021, 1,624 email responses were received (from more than 15,000 sent). Fernandez referred to this ongoing study when he spoke last month at the ICAEW 2021 Business Valuation Conference.

Average UK risk-free rates in May were 1.3% (with a lower 1.0% median). The UK’s rate is higher than most Scanadanavian and European nations, where rates in the 0.5%-to-0.9% range are more common. Given international conditions, respondents from Switzerland reported a negative RFR.

In the paper, the authors make these observations:

- Most previous surveys have been interested in the expected MRP, but this survey asks about the required MRP. Still, the return to market equity rate in the UK has trended toward a low point of 6.8% currently. Last year, it was 6.9%, compared to 6.9% in 2020 and 8.3% in 2019.

- Practitioners in South America report the highest required return rates—Venezuela led all countries, followed by Argentina.

- For European countries, many respondents use a risk-free rate higher than the yield of the 10-year government bonds; and

- The coefficient of variation (standard deviation/average) of the risk-free rate is higher than the coefficient of variation of MRP for the euro countries.

Pablo Fernandez, the professor in the department of financial management at the University of Navarra—IESE Business School in Spain, has over 200 papers published on SSRN, many of them related to valuation. He currently ranks first in all-time downloads on the 25-year-old research site. |

|

What are ‘reasonable’ requests for business valuation documentation from HMRC?

HMRC have generally argued that, once they reasonably establish an initial case against a taxpayer, the burden of proof passes to the taxpayer—and their financial experts. In practise, this can mean requests for reasonable information that seem to be, well, unreasonable.

The UK courts have been inconsistent in their treatment of burden of proof claims, and, last month, the First-Tier Tribunal (FFT) Tax Chamber (Judge Robin Vos) issued a new decision laying the burden of proof reasonably required under a taxpayer notice squarely at the feet of HMRC alone. In Perring v HMRC [2021] UKFTT 110 (TC), the FTT rejected HMRC’s “established initial case” argument, providing some protection for all financial experts who prepare fiscal reports.

The appellant’s expert was Gary Brothers of The Independent Tax and Forensic Services LLP. The decision can be viewed here. Of particular interest to business valuers is the analysis of inconsistent First-Tier burden-of-proof decisions in sections 58-65. The judge’s response to the appropriateness of the individual requests for information about tax liabilities from payments within a pension scheme begin in Section 109, and these offer new guidance to experts facing tax notices. |

|

Dates for your diary

23-24 August: Excel Modelling—Investment Appraisal, Valuation, and Business Cases, ICAEW live online, 09:30-12:30 BST

13-16 September: IMAA's Damodaran on Valuation, live online (repeated 8-11 November)

21-29 September: Practical Business Valuation, ICAEW live-online, four days, 09:30-12:30 BST

24-26 October: ASA International Conference, Las Vegas and online

27-29 October: IVSC Annual General Meeting, programme and format information to come

|

Want to share a news item? Have feedback or comments? Please contact

David Foster at ukeditor@bvresources.com. |

|

|

|

Business Valuation Resources, LLC

111 SW Columbia Street, Suite 750, Portland, OR 97201 U.S.A.

+011-503-479-8200 | info@bvresources.com

© 2021. All rights reserved.

|

|