|

|

BVWire—UK is a free service from BVR focusing on the business valuation profession in the United Kingdom. We offer news and perspectives from valuation thought leaders, the High Courts, HMRC, the standard-setters, ICAEW, RICS, and more.

Please be in touch with your perspectives, news, and ideas—and pass this issue along to colleagues (complimentary sign-up instructions are here).

|

Global intangibles lost 8% in value this year

Business valuers recognise that intangibles present individual ‘facts and circumstances’ challenges. Some intangibles appear on the balance sheet; many do not. And IFRS 3, even without the proposed amortisation changes, does not fully report the current value of acquired or created intangibles (reported intangibles can only retain value or increase, but increasing the operational value of intangibles is generally a strategic goal).

One place to look for benchmarks is GIobal Intangible Finance Tracker (GIFT) from Brand Finance.

‘GIFT 2019,’ released last month, takes issue with accounting standards (again) since they do not reflect fair value. David Haigh, CEO of Brand Finance, writes:

This seems bizarre to most ordinary, non-accounting managers. They point to the fact that while Smirnoff appears in Diageo’s balance sheet, Baileys does not. The value of Cadbury’s brands was not apparent in its balance sheet and probably not reflected in the share price prior to Kraft’s unsolicited and ultimately successful contested takeover of that once great British company.

Financial statements would improve immensely if the bulk of intangible value creation, currently undisclosed, were reported. To put this in perspective, Brand Finance estimates the global value of undisclosed intangible assets to now surpass US$35 trillion. Compare that to Aramco’s new market float valued (at the moment of writing) at US$2 trillion. No wonder analysts struggle.

What can business valuers learn from ‘GIFT 2019’?

- These assets declined in value a disturbing 8% compared to last year. The decline is dramatic—and the first decline of any magnitude since 2011. Enterprise value during the same period went up 2% (the smallest increase in the total worth of the world’s publicly traded companies since 2011), and reported intangible assets increased 7%. ‘GIFT 2019’ emphasises ‘this type of reduction is normally only recorded in years of recession’ and suggests ‘key sectors have lost momentum.’

- Even for intangibles disclosed via acquisition, the overuse of goodwill weakens the quality of financial reporting. In one of the best ‘I told you so’ examples of the year, Brand Finance senior consultant Annabel Brown writes of her report last November identifying Debenhams, Dixons Carphone, Pets at Home, and Thomas Cook as UK enterprises with high booked goodwill vs enterprise value. ‘Since that article was released, Debenhams have narrowly avoided administration, Dixons Carphone has faced a 22% profit slump, Pets at Home has witnessed a surprising revival … and hopefully no readers recently booked a holiday with Thomas Cook.’ (That must have been an enjoyable sentence for Brown to write.)

- The ranking of companies by total intangible value changes completely when undisclosed values are included. At the top, you get Microsoft, Amazon, Apple, and Alphabet. If the analyst looks only at disclosed intangibles, you get a lower-multiple segment of the economy driven by the big acquirers—AT&T tops the list, followed by Anheuser-Busch InBev, Comcast, and British American Tobacco. Smaller enterprises are less likely to have major internally generated brand values, but the trend still follows that higher-valued companies tend to have higher undisclosed intangibles.

|

|

|

KPMG Germany offers updated cost of capital study—and database of IFRS impairment test WACC results

KPMG Germany collected WACC results from 312 companies in Germany, Austria, and Switzerland for its 14th edition of the ‘Cost of Capital Study,’ concluding that the average WACC across industries remains at 6.9%. This is the same result as the last four editions of the study, but authors Dr. Marc Castedello and Stefan Schöniger (partners at KPMG AG Deal Advisory) express concern that this might be the ‘calm before the storm’ of regulatory interventions, scarcity of resources, climate change, further digitalisation of business models, and, of course, Brexit and the US-China scheme.

KPMG also makes WACC data available (for 150 countries) via their Valuation Data Source service.

Some further highlights of their new report:

- After an increase last year, the average risk-free rate remains nearly constant, at 1.2%—until recent months;

- The average market risk premium remains stable, at 6.5%;

- The highest unlevered beta factors were applied by the automotive and technology sectors; and

- The average cost of debt increased 0.1%, to 2.9%.

|

|

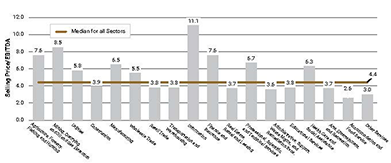

Median EBITDA multiple now 4.4x for small and medium enterprises

The median selling price/EBITDA multiple across all industry sectors is 4.4x, according to the 4Q 2019 DealStats Value Index (DVI). As the graph below shows, EBITDA multiples are highest for the information sector (11.1x) and the mining, quarrying, and oil and gas extraction sector (8.5x). Meanwhile, the lowest EBITDA multiples are in the accommodation and food services (2.6x) and the other services sectors (3.0x).

Click on image to view full size

The DealStats Value Index (DVI) summarises valuation multiples and profit margins for private companies that were sold over the past several quarters. The DVI is a quarterly newsletter and is complementary with a subscription to DealStats. |

|

Reminder: register for annual 2020 HMRC Shares and Assets Valuation Fiscal Forum by 14 January 2020

Business valuers who wish to attend the forum this year should notify Helen Malone by close of business on 14 January 2020. The same applies for any BVWire—UK reader who wishes to propose an agenda item or topic of conversation.

The year’s meeting (the first since October 2018) will be hosted at RICS (Parliament Square, London) commencing 25 February 2020 at 1.00 p.m.

One topic already included for discussion in February is the recent First Tier Tribunal of the Tax Chamber’s Vantis Tax Limited decision (TC07404). |

|

Study of large public projects confirms public/private value differences result from a ‘tax wedge’

Richard Brealey and Ian Cooper of London Business School, along with Michel Habib of the University of Zurich, have published a new study on taxes and value in the public sector. The study, published in the Journal of Business Finance & Accounting, establishes ‘the existence of a tax-induced wedge’ between private- and public-sector financing of huge capital projects such as toll roads or power plants ‘because taxes are a cost to the private sector but are only a transfer to the public sector.’ They conclude that this leads investors to more highly valued private enterprises with rapid tax depreciation, high debt capacity, and low risk.

While these cost of capital analyses are uncommon for most BVWire—UK readers, the study is helpful since it supports the practice of most business valuators when they assign higher values and lower cost of capital conclusions to private assets with these same characteristics. The study also provides mathematics to compare private investment tax shields with the UK Treasury’s present value project evaluation techniques. |

|

Dates for your business valuation diary

HMRC Shares and Assets Valuation Fiscal Forum, 25 February 2020, London

ICAEW Practical Business Valuation, 16-17 March 2020, London; 14 and 26 May 2020, London; 9 and 29 July 2020, London; 9 and 19 November 2020, London

ICAEW Business Acquisition & Due Diligence, 22 April 2020, London

73rd CFA Institute Annual Conference, 17-20 May 2020, Atlanta |

Our thanks to Marianne Tissier, Andrew Strickland, and Nick Talbot for their valuable contributions to BVWire—UK.

Want to share a news item? Have feedback or comments? Please contact David Foster (executive editor) at ukeditor@bvresources.com or +011-917-741-3853. |

|

|

|

Business Valuation Resources, LLC

111 SW Columbia Street, Suite 750, Portland, OR 97201 U.S.A.

+011-503-479-8200 | info@bvresources.com

© 2019. All rights reserved.

|

|